Essential bookkeeping reports every business owner should know

Did you know, according to the Australian Bureau of Statistics, that within the first three years, approximately 60% of small businesses fail due to poor financial management? It's a staggering statistic that highlights the critical role of bookkeeping services in business success. In today's fast-paced and competitive market, having a solid understanding of your company's financial health is essential for making informed decisions and ensuring long-term stability. That's where bookkeeping reports are essential.

In this blog, we will explore the essential bookkeeping reports that every business owner should know. These reports provide valuable insights into cash flow, profit and loss, assets and liabilities, and more. By keeping track of these reports, you can take control of your finances, drive growth, and avoid the common pitfalls that lead to business failure. Get ready to unlock the secrets of effective bookkeeping and propel your business towards success.

Key takeaways

Bookkeeping reports are crucial financial documents that provide insights into a company's financial health.

Essential bookkeeping reports include the Profit and Loss Statement, Balance Sheet, Cash Flow Statement, and more.

Accounting software plays a crucial role in generating bookkeeping reports accurately and efficiently.

CleanSlate helps businesses by generating accurate and reliable bookkeeping reports, enabling informed financial decision-making and promoting growth.

Bookkeeping reports: Understanding the basics

Bookkeeping reports are a crucial component of any company's accounting and finance departments. These reports consist of a record of all financial transactions that have taken place within a certain period, such as a month or a fiscal year. With the help of bookkeeping reports, businesses can track their revenue and expenses, monitor cash flow, and make informed decisions based on financial data.

These reports are also used to prepare tax returns and to provide financial statements to investors, lenders, and other stakeholders. A well-maintained set of bookkeeping reports is imperative for the smooth operation and success of any business, regardless of its size or industry.

Importance of bookkeeping reports

Bookkeeping reports, or Accounting reports, are really important for many reasons. They're not just about taxes. These reports help managers understand what's happening in different parts of a business so they can make good decisions to make more money.

There are other situations where accounting reports are really useful too. For example:

-

Figuring out how much a business is worth:

These reports help determine the value of a business when someone wants to buy it or invest in it.

-

Getting a loan for a small business:

When a business wants to borrow money, the reports show the lender how financially stable and healthy the business is. This helps the lender decide if they should give the loan and what the terms should be

-

Deciding on the right insurance:

The reports help figure out what kind of insurance a business needs and how much coverage is necessary.

For bigger companies, accounting reports are also important for showing shareholders how the company is doing financially. The reports give shareholders a clear picture of the company's financial status and how well it has been doing lately.

Top 5 essential business reports every business owners should be aware of

-

Profit and loss statement:

A Profit and loss statement (P&L), also known as an income statement or statement of operations, is a financial document that summarizes a company's revenues, expenses, and resulting profits or losses during a specific time period. It offers insights into a company's ability to generate sales, manage expenses, and ultimately create profits. The P&L statement is based on accounting principles such as revenue recognition, matching, and accruals, which distinguish it from the cash flow statement.

The structure of income statements typically covers a specific time frame, such as a month, quarter, or fiscal year. It includes various categories, such as:

- 1. Revenue (or Sales):

- The total amount of money generated from selling goods or services.

- 2. Cost of goods sold (or Cost of sales):

- The expenses directly associated with producing or delivering the goods or services being sold.

- 3. Selling, general & administrative (SG&A) expenses:

- Overhead costs related to the day-to-day operations of the business.

- 4. Marketing and advertising:

- Expenses incurred for promoting the company's products or services.

- 5. Technology/research & development:

- Costs associated with developing new technologies or conducting research.

- 6. Interest expense:

- The cost of borrowing money or paying interest on loans.

- 7. Taxes:

- The amount of taxes owed by the company based on its profits.

- 8. Net income:

- The final result after deducting all business expenses from the revenue, representing the company's profit or loss.

-

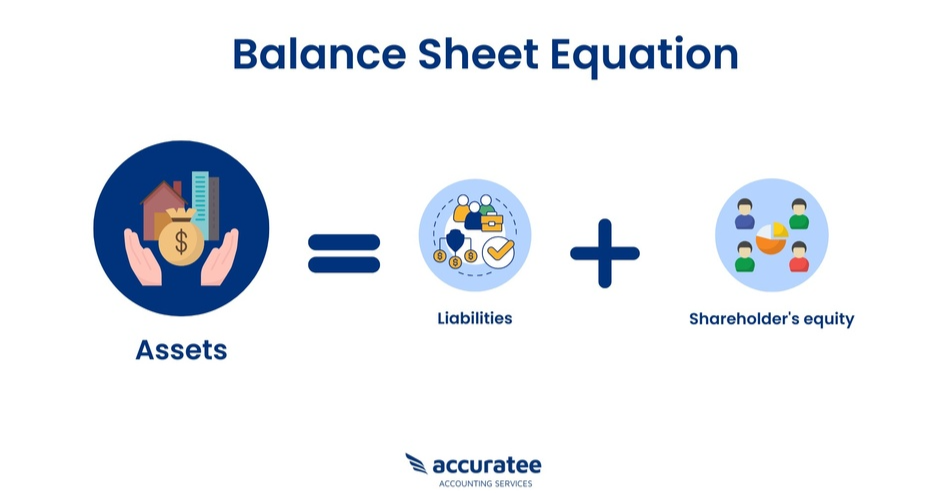

Balance sheet:

A balance sheet is a financial statement that provides a snapshot of a company's financial position at a specific point in time. It consists of two main sections: assets and liabilities.

Assets represent what the company owns, such as cash, inventory, equipment, and investments. Liabilities, on the other hand, represent the company's obligations and debts to external parties, such as loans, accounts payable, and accrued expenses.

The balance sheet equation shows that a company's assets are funded either by borrowing (liabilities) or by investments from shareholders (equity). Shareholder's equity is the residual interest in the company's assets after deducting liabilities. It represents the net worth or ownership claim of the shareholders.

The balance sheet helps stakeholders assess the financial health of a company by evaluating its liquidity, solvency, and overall financial stability. It enables investors to gauge the company's ability to meet short-term obligations and its long-term financial viability. By comparing balance sheets from different periods, stakeholders can track the company's growth, analyze trends, and make informed decisions.

Furthermore, the balance sheet serves as a reference for creditors to assess the creditworthiness of a company when considering loan applications. It provides insights into the company's assets and liabilities, helping creditors evaluate the risk associated with lending funds to the company.

-

Cash flow statement:

A cash flow statement is a financial statement that provides an overview of the cash inflows and outflows within an organization during a specific period. It is a crucial tool for managing finances and evaluating the financial health of a company.

The statement is divided into three main sections: operating activities, investment activities, and financial activities.

The operating activities section showcases the cash generated or used in the company's core operations, such as revenue from sales and payments for expenses like wages, taxes, and inventory.

The investment activities section reflects cash flows related to the purchase or sale of assets, including property, plant, and equipment. It also includes capital expenditures and investments.

The financial activities section records cash flows associated with financing, such as obtaining loans, issuing stocks, and paying dividends. This section helps analyze the company's interactions with owners and creditors.

By analyzing cash flow statements, businesses can gain insights into their spending patterns, maintain an optimum cash balance, focus on cash generation, and make informed decisions for short-term planning.

Positive cash flow is desired to meet financial obligations without relying heavily on borrowing. Negative cash flow, on the other hand, occurs when outgoing cash exceeds incoming cash and may require external financing to cover the shortfall.

-

Accounts receivables and payables aging report

Accounts Receivable (AR) and Accounts Payable (AP) aging are key financial reports providing insight into a company's cash flow and financial health.

AR Aging is a report that organizes receivables (money owed to the company) based on the length of time invoices have been outstanding. It’s segmented typically into 30-day buckets (e.g., 0-30 days, 31-60 days, etc.), providing a clear picture of the company's cash inflow. For example, if a business sees that a significant portion of its receivables are over 90 days due, it indicates that customers are paying late, posing potential credit risks.

In contrast, AP Aging organizes a company's bills based on their due dates. It helps manage outgoing cash flow by identifying which invoices are due in the present month, the following month, etc. For example, a car wash business may see a cleanser bill due within 30 days in the first bucket, and a scheduled equipment repair bill due next month in the second bucket.

AR aging aids in estimating allowance for doubtful accounts, preventing income overstatement, while AP aging allows prioritizing and scheduling payments to suppliers efficiently. Thus, both reports are crucial for a company's fiscal management and ensuring smooth operationBoth reports help businesses in financial planning and risk assessment.

-

Budget vs. actual report

A budget vs. actual report is a financial analysis tool that compares the projected budgeted amounts with the actual financial results. It combines an income statement with a budget income statement, allowing organizations to assess the accuracy of their financial planning and control.

The report provides both dollar and percentage comparisons between the budgeted and actual figures, enabling a detailed analysis of income and expenses. By reviewing the variances, organizations can identify areas where they exceeded or fell short of their budgeted expectations.

This report is highly beneficial for evaluating the financial performance and making informed decisions. It helps in understanding how closely the actual income and expenses align with the budgeted amounts, providing insights into areas of financial strength or weakness. By tracking these variances, organizations can adjust their future budgets, optimize resource allocation, and implement strategies to improve profitability and operational efficiency.

The report can be customized to include statistical accounts, allowing for comparisons beyond traditional financial data. By incorporating additional metrics such as headcount or production quantities, organizations gain a comprehensive view of their performance.

For example:

A fictional company may have $1 million in revenue, $600,000 in cost of goods sold, $200,000 in SG&A expenses, $50,000 in marketing and advertising expenses, $30,000 in technology/research & development costs, $10,000 in interest expense, and $100,000 in taxes. After subtracting all expenses from revenue, the net income would be $10,000, indicating a profit for that specific period.

How can accounting software assist in generating bookkeeping reports, and what features should one look for in such software?

Accounting softwares plays a crucial role in generating bookkeeping reports, providing businesses with accurate and timely financial information. When considering cloud-based accounting software, it's important to look for specific features that facilitate efficient report generation for bookkeeping purposes. These include:

-

Report customization:

Does the software offer the ability to customize bookkeeping reports based on the specific needs of the business? This allows businesses to tailor the reports to include relevant information and key performance indicators.

-

Time frame adjustments and comparisons:

Can the software adjust time frames and compare current bookkeeping results with previous periods? This feature enables businesses to analyze trends, identify patterns, and evaluate their financial performance over time.

-

Account filtering and categorization:

Does the software allow for selective inclusion or exclusion of specific accounts or line items in bookkeeping reports? This capability enables businesses to focus on relevant data and highlight specific areas of interest.

-

Notes and annotations:

Is there a feature to add notes or annotations to bookkeeping reports? This allows businesses to provide explanations for unusual transactions or highlight important details for further analysis.

-

Real-time updates:

Does the software provide real-time data synchronization, ensuring that bookkeeping reports are continuously updated with the latest financial information?

By considering these features, businesses can select accounting software that streamlines the process of generating accurate and customizable bookkeeping reports. Such software empowers businesses to gain insights into their financial performance, make informed decisions, and effectively manage their bookkeeping processes.

Expert Bookkeeping at Your Fingertips!

How CleanSlate helps in generating essential bookkeeping reports?

Small business owners face the challenging task of understanding their financial status while simultaneously driving business operations. Generating and interpreting bookkeeping reports is a complex task, especially for those without a finance background. Recognizing this, CleanSlate steps in as a secure and efficient solution to your bookkeeping needs.

-

Data security:

In an era where data breaches are becoming increasingly common, security is paramount. CleanSlate is ISO 27001 certified, indicating our commitment to stringent information security management systems. We implement robust security measures, ensuring your sensitive financial data remains confidential and secure. You can trust CleanSlate with your financial data, knowing it is protected by globally recognized security standards.

-

Reliability and accuracy:

We deliver accurate and reliable outsourced bookkeeping services. Our team utilizes advanced accounting softwares like (Xero and Quickbooks), and employs meticulous cross-checking processes to ensure error-free bookkeeping reports

-

Time efficiency:

By outsourcing your bookkeeping tasks to CleanSlate, you free up valuable time and resources to focus on core business operations.

-

Tailored financial insight:

We understand each business is unique and tailor our services accordingly to provide relevant, comprehensive, and insightful reports.

-

Scalability:

As your business grows, so does your financial complexity. CleanSlate’s services scale with your business, accommodating growth and expansion without compromising the quality or efficiency of reports.

-

Cost-effective:

CleanSlate offers a more affordable solution than hiring a full-time, in-house bookkeeper, providing professional bookkeeping services at a fraction of the cost.

-

Proactive financial management:

Beyond just generating reports, we provide a detailed analysis of your financial status, identifying trends, spotting potential issues, and suggesting strategic solutions.

Choosing CleanSlate for your bookkeeping needs means you gain a secure and dedicated financial partner. We help you understand your financial health, fostering informed decision-making, and ultimately driving the success of your business.

Conclusion

Keeping up with your bookkeeping can have a drastic effect on the success of your business. Utilizing and understanding the reports outlined in this blog post can help you make more informed decisions, stay organized, and make sure that all necessary information is available at any given time. With this knowledge, you can confidently set up accurate financial goals for yourself and take charge of your business finances.

At CleanSlate, our bookkeeping professionals are on standby to provide guidance and support during any of these processes. Make sure to take advantage of their assistance when needed. Many times it’s just what you need to feel confident about your funds! With the right strategy in place, you will be able to make more significant investments into your business and watch it grow exponentially.

So what are you waiting for? Start gathering essential reports today and take charge of your business finances. Contact us or reach out today!