Superannuation guarantee: Are you ensuring compliance with employee retirement contributions?

Introduction:

Superannuation guarantee and compliance play a crucial role in ensuring the financial security of employees during their retirement years. As an employer, it is essential to understand and meet your obligations when it comes to employee superannuation contributions.

In this blog post, we will delve into the significance of superannuation guarantee compliance and provide you with valuable insights to ensure that you are meeting your responsibilities.

Whether you are a small or medium-sized business owner in Australia, this post aims to guide you in navigating the complexities of employee retirement contributions and help you secure a prosperous future for your workforce.

Key takeaways

Superannuation guarantee is a legal requirement for employers in Australia to contribute to their employees' retirement savings, ensuring their financial security.

Compliance with superannuation contributions involves understanding contribution rates, accurately calculating and paying super, and following compliance guidelines and deadlines.

Non-compliance with employee retirement contributions can lead to penalties and reputational damage for businesses.

Seeking professional assistance from accounting and bookkeeping services, such as CleanSlate, can simplify the compliance process, ensure accurate reporting, and help businesses meet their superannuation obligations effectively.

What is a superannuation guarantee?

Superannuation guarantee refers to the compulsory contributions made by employers on behalf of their employees towards their retirement savings. It is designed to help individuals accumulate sufficient funds to support themselves when they retire. The significance of a super guarantee lies in its ability to create a reliable and sustainable income stream for employees during their non-working years.

What is the superannuation guarantee percentage?

Employers in Australia have legal obligations to comply with the super guarantee laws. Currently, the superannuation guarantee rate is 10.5% of an employee's earnings.

However, it is important to note that this rate will increase to 11% from 1 July 2023. Additionally, the rate will gradually increase by 0.5% each year until it reaches 12% in 2025. It is crucial for employers to stay updated with these changes and ensure timely payment of the correct contribution amounts to their employees' chosen super fund.

Example:

Let's consider an employee, Sarah, with monthly eligible earnings of $4,000.

To calculate Sarah's superannuation guarantee contribution for a specific month:

Superannuation guarantee contribution = Employee's ordinary time earnings x superannuation guarantee rate

For the current rate of 10.5%: Superannuation guarantee contribution = $4,000 x 10.5% = $420

In this example, the employer would contribute $420 to Sarah's chosen super fund for that particular month, representing 10.5% of her monthly earnings.

Who is eligible for a superannuation guarantee?

The superannuation guarantee applies to most employees working in Australia. Generally, the following criteria determine eligibility for the super obligations:

-

Age:

Employees must be at least 18 years old or over and be earning $450 or more (before tax) in a month to be eligible. However, there is no age limit for employees who are classified as eligible temporary residents.

-

Employment type:

Full-time, part-time, and casual employees are generally eligible for the super guarantee. This includes employees on temporary work visas and certain contractors who are considered employees for superannuation purposes.

-

Earnings:

Employees must earn a minimum of $450 (before tax) in a month from a single employer to be eligible for superannuation guarantee contributions. This threshold applies to each individual employer, so if an employee works for multiple employers, each employer must separately contribute once the threshold is met.

There may be some exceptions and specific circumstances that impact eligibility. For instance, employees under the age of 18 may need to meet additional requirements.

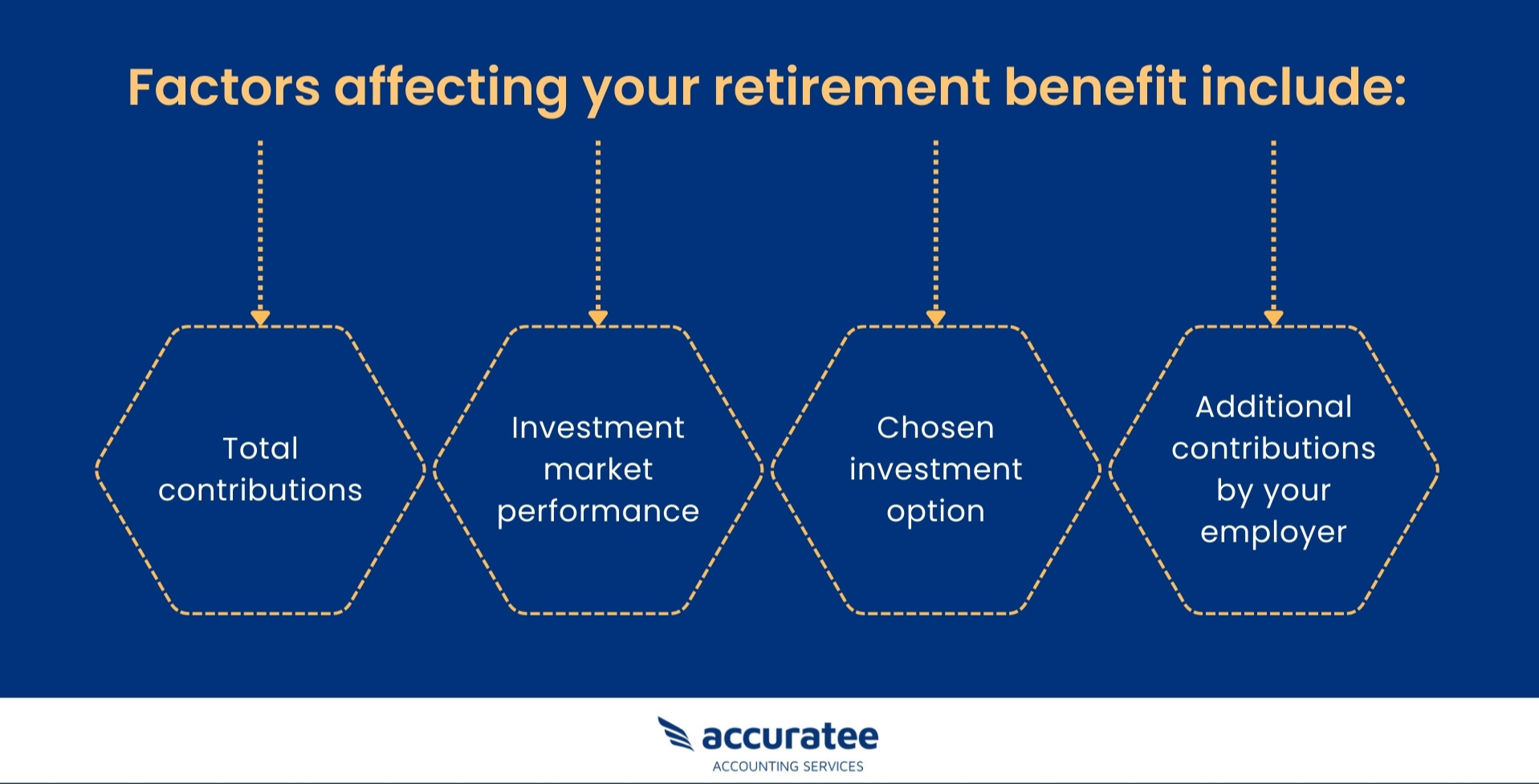

What are the benefits of superannuation contributions for employees?

Superannuation offers numerous benefits to employees, making it an essential aspect of their overall financial well-being. It provides a means to accumulate savings over their working lives, ensuring they have sufficient funds for retirement. With the increase in contribution rates, employees will be able to build a more robust fund.

Superannuation also offers tax advantages, as super guarantee contributions are typically taxed at a lower rate compared to regular income. Furthermore, employees can choose investment options to grow their superannuation savings over time.

By understanding the significance of super guarantee and the changing contribution rates, employers can fulfil their legal obligations and contribute to the financial security of their employees' retirement years.

Ways in which employers can meet the obligations for employee retirement contributions.

By ensuring compliance with employee retirement contributions you not only fulfil legal requirements but also contribute to their future savings.

-

Understand your responsibilities:

Familiarise yourself with your responsibilities as an employer regarding superannuation contributions. Know the current contribution rate, eligibility criteria, and reporting requirements.

-

Calculate correctly:

Accurately calculate superannuation contributions based on the employee's ordinary time earnings and the applicable contribution rate. Exclude overtime pay when calculating contributions.

-

Make timely contributions:

Ensure you make super payments at least quarterly and within 28 days after the end of each quarter. Pay attention to payment deadlines to avoid penalties and interest charges.

-

Keep accurate records:

Maintain detailed records of super guarantee contributions, eligible earnings, and relevant documentation. This includes employee information, payment records, and any adjustments made.

-

Provide choice of fund:

Give your employees the opportunity to choose their own super fund. Provide them with the necessary information and ensure their defined benefit fund meets the Superannuation Industry (Supervision) Act 1993 requirements.

-

Communicate with employees:

Regularly communicate with your employees about their superannuation and the payments you are making on their behalf. Provide them with relevant information, updates, and access to their superannuation statements.

-

Keep up with legislative changes:

Stay informed about any changes to super rules, contribution rates, and compliance requirements. Regularly review and update your processes to ensure ongoing compliance.

-

Pay super online:

Under the SuperStream standards, it is mandatory to pay superannuation contributions using an online payment system, such as a super clearing house, which offers dedicated support for setting up and managing super payments. Visit government websites for updates.

-

Follow the onboarding rule for new employees:

Offer new employees a choice of super fund by providing a superannuation standard choice form within 28 days of their employment commencement. If they do not choose a fund, you must pay their super contributions into their stapled super fund or, if they don't have one, into your business's default fund.

-

Manage reportable super contributions:

Report any additional super contributions you make for your employee to the Australian Taxation Office (ATO) website. This includes amounts deducted from employees' pre-tax income, such as salary sacrificed amounts. Reporting can be done through Single Touch Payroll (STP) or on the employee's annual payment summary.

Expert Bookkeeping at Your Fingertips!

What are the different types of superannuation in Australia?

-

Industry super funds:

Industry super funds are established to cater to specific industries, such as construction, healthcare, or hospitality. They are typically not-for-profit funds and are governed by employer and employee representatives. These funds aim to provide competitive investment returns and low fees.

-

Retail super funds:

Retail super funds are offered by financial institutions such as banks and investment companies. They are open to the general public and operate for profit. Retail funds offer a range of investment options and may provide additional services such as financial advice.

-

Corporate super funds:

Corporate super funds are established by employers for their employees. They are generally not open to the public and are designed to meet the specific needs of the company and its workforce. Corporate funds may offer tailored investment options and benefits unique to the organisation.

-

Self-managed super funds (SMSFs):

SMSFs are private super funds managed by individuals or a small group of trustees. They provide individuals with greater control over their investment decisions and savings. SMSFs require active management, compliance with regulations, and the responsibility of accounting and reporting.

-

Public sector super funds:

Public sector super funds are specifically designed for employees in the public sector, including government employees and members of certain public organisations. These funds offer benefits and features tailored to public sector employees.

How can employers help in optimising superannuation contributions?

Employers should consider the following strategies to help employees maximise their super guarantee funds:

-

Maximise superannuation benefits:

Business owners should encourage employees to contribute more than the minimum required amount to their stapled super fund. By doing so, they can take advantage of potential tax benefits and boost their savings. Emphasise the importance of taking an active role in their superannuation to secure a comfortable future.

-

Salary sacrifice and voluntary contributions:

They can explain the advantages of salary sacrifice, where employees can contribute a portion of their pre-tax income directly into their super fund. This strategy not only reduces their taxable income but also allows for potential tax savings. Encourage employees to consider making additional voluntary payments from their after-tax income to grow their super fund further.

-

Investment choices and long-term planning:

Furthermore, employers can educate employees about investment options within their super fund. Provide information on diversification, risk management, and potential returns to help them make informed decisions. Encourage long-term planning by highlighting the advantages of staying invested and regularly reviewing their investment strategy as they approach retirement.

By implementing these strategies, employees can optimise their superannuation contributions and enhance their retirement prospects.

How can employees maximise their retirement savings with voluntary super contributions?

Voluntary super contributions offer a powerful way to grow retirement savings. By making additional payments, even small amounts can accumulate over time. Employers can play a crucial role in educating their employees about the benefits of voluntary contributions.

They can provide information on salary sacrifice options, where employees can direct a portion of their pre-tax pay into their super accounts. The payments, known as concessional contributions, are taxed at 15%, which is often lower than the employees' marginal tax rate. However, it's important to note that there is a limit to how much extra can be contributed. The combined total of employer and salary sacrificed contributions must not exceed $27,500 per financial year.

Additionally, employees can also make after-tax contributions, known as non-concessional contributions, up to $110,000 per financial year. Employers can educate their employees about these contribution limits and provide guidance on maximising their contributions within these thresholds.

Furthermore, employers can inform their employees about government initiatives such as the low-income super tax offset (LISTO) for those earning $37,000 or less, and the co-contribution scheme for low to middle-income earners. These initiatives provide additional financial incentives for making voluntary contributions.

How can online accounting and bookkeeping services help?

Professional online accounting and bookkeeping services, like those offered by CleanSlate, provide invaluable assistance in ensuring compliance with employee retirement contributions. Here's how CleanSlate can help:

-

Accurate record-keeping:

We maintain meticulous records of superannuation guarantee contributions, including employee information, contribution amounts, and payment records. This ensures that all data is organised and readily accessible for compliance purposes.

-

Reconciliation of superannuation accounts:

Our firm reconciles superannuation accounts to ensure that contributions are correctly allocated to employees' super funds. This helps identify any discrepancies and ensures accurate reporting.

-

Stay updated with compliance requirements:

We stay up to date with changes in legislation and compliance requirements related to superannuation. This ensures that businesses are aware of any regulatory updates and can adjust their processes accordingly.

-

Expert guidance:

CleanSlate provides expert advice on meeting superannuation obligations. We have in-depth knowledge of compliance rules and can guide businesses on the best practices to follow. This includes advice on calculating contributions, handling salary sacrifice, and managing compliance due dates.

-

Navigate complex processes:

Complying with superannuation requirements can be complex, but CleanSlate simplifies the process for businesses. We assist in navigating through various compliance procedures, ensuring that businesses fulfil their obligations accurately and efficiently.

Ending note

Ensuring compliance with employee retirement contributions is vital for businesses. By partnering with CleanSlate, a leading online accounting and bookkeeping service provider, businesses can benefit from their specialised knowledge and expertise. Our accounting firm helps streamline compliance processes, reduce errors, and ensure precise management of employee retirement contributions.

Take action now to secure a prosperous future for your business and employees. Prioritise compliance, and trust CleanSlate for professional assistance.